GEA4: Supporting Clean Energy or Subsidizing Poor Siting Decisions?

- September 30, 2025

- 0

Latest development on Green Energy Auction Program Round 4 (GEA-4)

The fourth round of the Philippines’ Green Energy Auction (GEA‑4) was formally announced in March 2025, with its Terms of Reference released to the public shortly thereafter. This latest auction represents a landmark in the nation’s renewable procurement, targeting approximately 10.7 gigawatts (GW) of new capacity across technologies such as ground-mounted, roof-mounted, floating solar, as well as onshore wind. For the first time, Integrated Solar and Energy Storage Systems (IRESS), which pairs solar installations with battery energy storage, was included to bolster grid flexibility and resilience.

Following a structured timeline, registration of qualified bidders took place in mid‑June, and 142 bidders were deemed qualified to participate in GEA-4. The auction proper was held on 2 September 2025, and the DOE had just released the preliminary results of accepted bids on 4 September 2025, with certificates of award to follow between late November and early January.

Attractiveness of GEA-4 as a route-to-market option for renewable energy

For many developers, the Green Energy Auction Program (GEAP) and its associated Renewable Energy Payment Agreement (REPA) is considered as one of the most attractive route-to-market options in the Philippines (you may learn more about Route-to-market options for Philippines renewables here).

From a project finance (PF) perspective, REPAs are highly attractive: they provide 20-year fixed-price offtake contracts with no exposure to nodal price volatility or line rental cost risk. Line rental costs are issues that frequently undermine revenue stability in the Philippines’ locational marginal pricing (LMP) system. For lenders, the predictability from the REPA translates into stronger debt service coverage ratios and lower perceived risk, particularly when compared to merchant or contract-for-difference (CfD) arrangements where revenue is partially exposed to market or delivery uncertainty.

However, the REPA structure is not without risk. Its primary downside is curtailment. Generators are only paid for actual delivered energy, meaning any system-induced curtailment directly reduces revenue. A second commercial risk lies in the performance bond mechanism: developers must meet their committed Delivery Commencement Date (DCD) or risk forfeiting a significant portion of their bid security. This makes execution risk (permitting delays, EPC bottlenecks, or grid interconnection setbacks) a material concern that must be carefully managed in the early stages of development.

Building on the above dynamics, GEAP tends to attract developers whose projects have limited merchant potential in WESM often due to grid-induced disadvantages such as lower nodal prices or high curtailment exposure. These conditions constrain the commercial viability of selling directly into the spot market. Similar to nodal markets in the US (e.g., CAISO and ERCOT), the Philippines imposes locational penalties on generators that connect in congested or saturated zones, effectively “punishing” poorly sited assets through adverse price signals or reduced dispatch. For such projects, GEAP (with its location-neutral tariff and insulation from nodal basis risk) serves as a crucial alternative route to market. Click here to read about how to pick the right place to build

Analysis on GEA-4 preliminary auction results – Solar and onshore wind

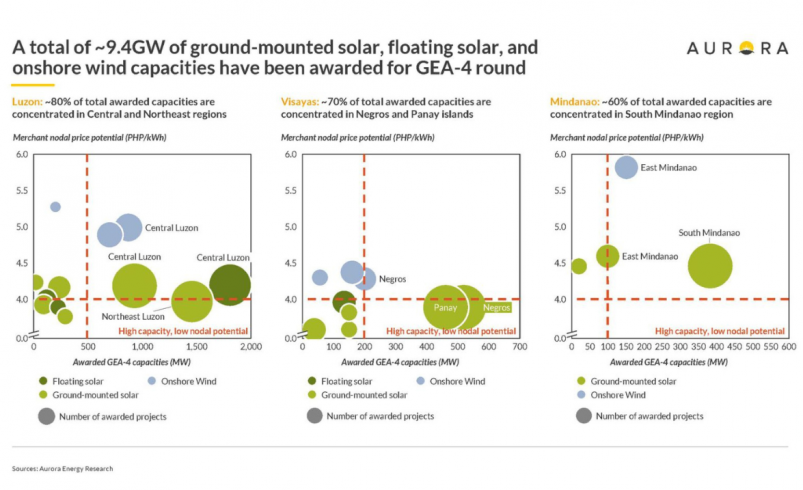

Based on preliminary results, a total of 111 renewable energy projects were awarded under GEA4, representing approximately 9.4 GW of new capacity across Luzon, Visayas, and Mindanao. Luzon dominated the awards with around 7 GW, of which nearly 80% is concentrated in Central and Northeast Luzon, which are areas already facing growing grid integration pressures. In the Visayas, about 1.9 GW was awarded, with Negros and Panay Islands accounting for roughly 70% of regional capacity. Mindanao saw the smallest allocation, with just 650 MW awarded, in which 60% of these capacities are concentrated in the South Mindanao region.

Two key implications emerged from the preliminary GEA-4 results. First, a significant share of awarded projects appears to have limited merchant potential, with siting concentrated in nodes prone to congestion and low nodal pricing—suggesting developers turned to GEAP as a hedge against weak spot market viability. Second, the GEA-All fund may face mounting pressure, as TransCo could struggle to recover payouts from WESM due to subpar capture prices at these nodes. This raises the likelihood of higher GEA-All surcharges for end-consumers over time.

Nodal potentials of awarded GEA-4 projects

According to Aurora’s GEA4 competitive benchmarking analysis, expected average solar capture prices at the nodal level ranged from 3.4–5.4 PHP/kWh, with regional averages of 3.8–4.9 PHP/kWh in Luzon, 3.4–4.6 PHP/kWh in Visayas, and 4.0–5.4 PHP/kWh in Mindanao. However, based on the preliminary list of awarded projects, Aurora estimates that capture prices of awarded projects would be notably lower, averaging 3.6–4.6 PHP/kWh, with regional averages of 3.8–4.2 PHP/kWh in Luzon, 3.6–4.0 PHP/kWh in Visayas, and 4.5–4.6 PHP/kWh in Mindanao. This suggests that projects with relatively weaker market fundamentals, i.e. those located at nodes with lower merchant value, were more leaning to win GEAP to secure offtake, reinforcing the view that GEA4 has acted as a safety net for commercially disadvantaged assets.

Moreover, projects with weaker market fundamentals are often more exposed to grid curtailment risk. The very condition that suppresses nodal prices, i.e. marginal cost of congestion, also heightens the likelihood of curtailment to these projects. In effect, these projects are being penalised by system design. If congestion worsens and transmission upgrades are delayed, the resulting bottlenecks can significantly erode project revenue, undermining even the security offered by long-term contracts, such as REPA.

Impact of GEA-4 procurement to GEA-all rates

The GEAP mechanism is indirectly funded by electricity consumers through the GEA-All charge, a surcharge collected via the electricity bill and administered by the National Transmission Corporation (TransCo). This charge functions similarly to the historical FIT-All mechanism used to support feed-in tariff projects, pooling funds to pay renewable energy developers the difference between the auction tariff and spot market prices. As with the FIT-All, GEA-All is regulated by the Energy Regulatory Commission (ERC), which reviews and approves the rates based on actual disbursements and forward-looking obligations.

Given the preliminary results of GEA-4 and assuming 100% fulfilment rates for GEA-5 (GEA-5 involves offshore wind—typically one of the costliest forms of renewable energy), Aurora Energy Research forecasts the GEA-All rate to gradually increase to a range between 0.45 – 0.49 PHP/kWh in the early 2030s. For comparison, the historical FIT-All rate has ranged between 0.04 – 0.25 PHP/kWh, this reflects a shift in installed capacity and market settlement prices over time.

Whether the Philippines requires offshore wind in the short to medium term remains an open question (and one that merits separate analysis). However, the actual GEA-All rate will depend on factors such as the fulfilment rates of GEA auctions and the bid prices submitted. If these fall short of expectations, the realised GEA-All rate could be lower than projected and may remain within a manageable range for consumers. For now, the design of the GEA-All framework ensures that costs are socialised while offering investors a stable route to market, provided projects can be delivered on time and within their auction price commitments.

About Aurora Energy Research

Aurora Energy Research is a global power market and grid analytics firm, specializing in providing more precious valuation with long-term nodal price forecasts for the Philippines power market. As of to-date, Aurora has supported over $45bn USD worth of project financing globally.