GEA-5: What defines success for the inaugural offshore wind auction?

- December 22, 2025

- 0

by Philipp Egli (Research Lead, Wider Asia, Aurora Energy Research)

A nation steps into offshore wind with high hopes and high stakes

When the Philippine government officially launched its inaugural offshore wind auction on 25 November 2025, it marked an important milestone on a long journey to harnessing its excellent renewables potential. Institutional actors from the Department of Energy (DOE) to the World Bank and Global Wind Energy Council as well as private developers have been working towards integrating offshore wind into the Philippines’ power mix for years. The fifth Green Energy Auction, or GEA-5, formally invites bids to build the country’s first utility-scale offshore wind farms. Officials have framed the auction as the beginning of a long-term shift toward a cleaner, more resilient power system, and they are treating the moment accordingly: not as a tentative pilot, but as the first round of a sustained offshore wind program intended to redefine the country’s energy future.

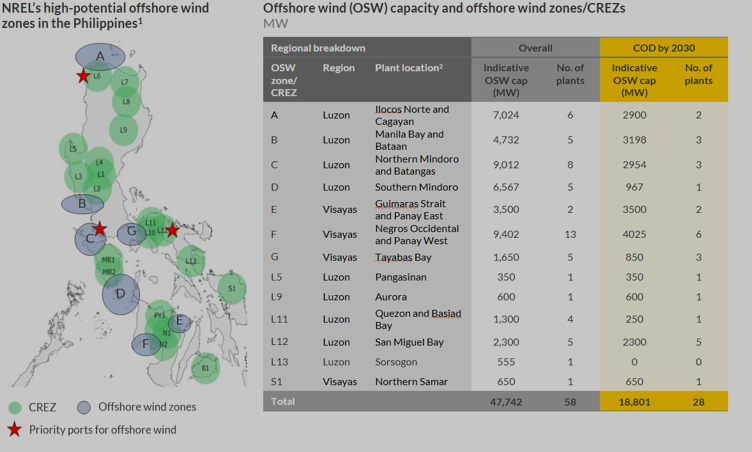

With perpetual coastal winds and large bodies of relatively shallow waters, offshore wind has tantalised Philippine policymakers and developers for years. The potential is vast—178 gigawatts according to the Department of Energy’s own numbers—but until now, that potential was out of reach. GEA-5 marks the first time the institutions, rules, and supporting structures have been brought to a point where large-scale projects can begin their march toward construction.

Yet even in its earliest hours, GEA-5 is defined as much by its challenges as its promise. The timeline is compressed. The financial stakes are high. And so are the expectations—within government, industry, and the public. The Philippines is wagering that it can push a sector to commercially operating reality within just a few years.

Institutions move in lockstep as policy ambition meets tight timelines

Part of what sets GEA-5 apart is the level of institutional coordination behind it. The Department of Energy, the Energy Regulatory Commission, the Philippines Port Authority and the National Grid Corporation of the Philippines are striving to synchronise their planning. This coordination underpins the government’s belief that the Philippines can move quickly enough to deliver first power from offshore turbines before the end of the decade.

The government’s confidence is codified in its schedule: bidder registration opens early in 2026, followed by an extensive pre-bid process and a live auction expected in the first half of the year. As winning bidders are announced shortly after, the clock starts ticking. In theory, the earliest projects could begin sending electricity to the grid is as soon as 2028—an extraordinarily tight horizon for a sector that, typically requires long development cycles, lengthy environmental reviews, and years of port and grid upgrades. Some of the early adopters in the Europe Union took the best part of a decade from award to construction.

To enable development, the government has also committed itself to significant infrastructure investment. Two key ports—a greenfield project in Camarines Norte and a redevelopment in Batangas—are intended to support offshore wind installation and maintenance. Transmission planners are accelerating work on major reinforcement corridors, particularly across the Visayas region and Bicol region, where offshore wind power is expected to accumulate. These upgrades are designed not only to support the first projects, but also to lay the groundwork for a sequence of future auctions.

The release of the preliminary GEA reference price on 12 December further demonstrates the institutional commitment. While the price cap at ~10.4PHP/kWh is roughly double last year’s average wholesale power prices, the implicit understanding is that offshore wind is a new frontier and that these front-runner projects are facing significant delivery risks which need an adequate reward potential.

Surprising tailwinds and expectable headwinds: no substitute for grid

The promise of offshore wind in the Philippines is immense, but so are the uncertainties confronting developers. A noteworthy tailwind comes in the form of a pragmatic attitude towards industrial policy. The sector enjoys the rare advantage of moving forward without local content mandates. Unlike other offshore wind markets that require developers to rely heavily on domestic supply chains — often yet to develop themselves — the Philippines has opted for an open model, allowing procurement from wherever it is most competitive. This decision could dramatically influence outcomes, particularly as Chinese manufacturers of wind turbine generators, the single most costly component, have entered global offshore markets with very competitive solutions. This flexibility could be decisive. For developers navigating the economics of a first-of-its-kind market, the ability to source equipment globally helps lower costs and expand participation.

Still, technology and hardware are only part of the calculus. The development landscape is dotted with risks, many of them inherent to early-stage offshore deployment. The absence of a fully consolidated marine spatial plan means not all potential conflicts between fisheries, shipping lanes, ecological zones, and national security uses have been fully resolved. Environmental permitting, while improving, remains a complex process involving multiple layers of national and local authorities. Meanwhile, seabed conditions in several high-potential zones pose engineering challenges, and there is still a dearth of bankable commitments on how and even where to build the domestic port infrastructure. Even when port upgrades eventually get underway, installation vessels and heavy-lift capacity remain scarce, while the vast pool of Filipino seafarers needs retraining to adapt to offshore wind.

An entirely expectable headwind is grid readiness. Several developers and the project finance community have clearly expressed their concern about grid and the risk of curtailment. Aurora Energy Research has built a power market and grid model and helps developers gauge the volume risk of curtailment under different scenarios. Assuming 100% delivery of capacity from GEA-4 and 5 would trigger up to 16% curtailment across swathes of the wind fleet in Visayas. While we do not expect such high delivery of GEA capacities, curtailment will affect developers unequally depending on location. Offshore developers are confident that they can find workarounds for logistical bottlenecks, but there is simply no substitute for grid.

With delays foreseeable, policymakers have attempted to lighten the load where possible. The auction design includes provisions for excusable delays, namely on the availability of grid or port infrastructure, acknowledging that timelines in offshore wind are not always under a developer’s control.

Source: WindEurope

A vast pipeline, but few truly ready to deliver early

From a distance, the Philippines looks like a hotbed of offshore wind development, with nearly fifty gigawatts’ worth of projects listed. But a closer look reveals a different reality: only a fraction of these can realistically compete in GEA-5. Many projects remain early in their life cycles, still lacking environmental permits, detailed feasibility studies, or grid connection assessments. Therefore, we expect only a fraction of the theoretical pipeline to participate and bid.

Within this narrower field are a mix of international and local players: global offshore wind specialists, longstanding Philippine energy developers, and ambitious newcomers. Some, including companies with sizeable portfolios on paper, may not yet have the maturity to enter the first auction. Others with fewer megawatts but more advanced preparatory work may find themselves rather competitive.

The government’s decision to adopt a hybrid evaluation framework—which weighs project readiness and grid integration alongside price—reflects this reality. Price remains the dominant factor, but non‑price elements now carry enough weight to reward developers who have invested in early groundwork. In this first auction, feasibility, permitting progress, and credible timelines may separate serious contenders from those whose ambitions exceed their preparations.

The road ahead: the long game of offshore wind

As the Philippines steps into offshore wind for the first time, the path forward will be shaped by competing forces: ambition and caution, optimism and uncertainty, vision and technical reality. The country has set itself a bold challenge—compressing years of development into a narrow window and doing so with limited precedent. It has also provided, through policy signals and infrastructure commitments, a strong foundation for eventual success.

Much will depend on how quickly the grid evolves and how the global supply chain responds to the Philippines’ call to action. Equally important will be whether the institutional resolve visible in GEA-5 can be sustained through successive rounds, especially as political cycles shift and the out-of-market support for offshore wind becomes more salient in retail tariffs through the GEA allowance.

How does success look like? Not simply awarding capacity, but kickstarting a cycle in which projects get awarded and delivered, within acceptable time frames, triggering domestic capacity building and cost-reductions in the supply chain, paving the way for future, larger deployments in a financially sustainable fashion. The winds that have long swept across the archipelago may soon power its future.

About

Aurora Energy Research is a global power market and grid analytics firm, specializing in providing more precise valuation with long-term nodal price forecasts for the Philippines power market. As of to-date, Aurora has supported over USD 45bn USD worth of project financing globally.

Reach out to [email protected] or inquire through our website if you’d like to know more. https://auroraer.com/global-presence/philippines

Image Source: WindEurope