Green Dreams, Bankable Schemes: How To Thrive In The Philippine Power Market

- May 19, 2025

- 0

By Patrick Tan, Head of Wider Asia, APAC at Aurora Energy Research

Developers, lenders, and investors eyeing the Philippine solar and wind sectors face a growing array of route-to-market strategies, each with its own blend of revenue certainty and risk. These include: (1) merchant trading through the Wholesale Electricity Spot Market (WESM), (2) corporate power purchase agreements (CPPAs), often via Retail Electricity Suppliers (RES), (3) power supply agreements (PSAs) with distribution utilities, and (4) participation in the Green Energy Auction Program (GEAP). Each model reflects distinct regulatory, commercial, and infrastructure dynamics, and understanding their nuances is critical for crafting a viable investment thesis.

Overview of the Philippine Power Market

The Philippine electricity system is divided into three pricing zones—Luzon, Visayas, and Mindanao—mirroring the nation’s geographic layout and grid fragmentation. Total generation in 2023 reached approximately 118 TWh, with 80% still coming from fossil fuels, primarily coal and natural gas. Renewables, such as hydro, geothermal, and solar, contribute the remaining 20%, which is a modest share despite vast potential.

Figure 1: Overview of the Philippine Power Market

The market operates under a nodal pricing system within WESM based on Locational Marginal Pricing (LMP). This method reflects the marginal cost of delivering energy to each grid node, factoring in system-wide conditions, line losses, and congestion. WESM trades in five-minute intervals and accounts for approximately 20% of total national electricity traded.

Complementing WESM are two newer mechanisms: the Reserve Market and the Renewable Energy Certificate Market (REM). The Reserve Market, launched in January 2024, enables real-time procurement of ancillary services—Regulation Up, Regulation Down, Contingency Reserve, and Dispatchable Reserve. The market has seen prices frequently hit regulatory caps due to limited market competition, although the commissioning of 2–3 GW of battery energy storage systems (BESS) is expected to stabilise the market. REM, operational since December 2024, supports voluntary REC trading under a 241.56 ₱/REC cap, offering an emerging source of green premium revenue for developers.

Figure 2: Philippines power market structure

Curtailment and Grid Constraints

Irrespective of market route, renewable projects in the Philippines face two structural challenges: economic curtailment and grid-induced curtailment. Economic curtailment arises when spot prices fall too low to justify dispatch—typically during midday solar peaks or off-peak demand periods. Grid curtailment stems from physical transmission limitations, particularly acute in high-renewable zones like Negros and Northern Luzon.

These risks can significantly erode project economics. While BESS co-location offers mitigation by enabling energy time-shifting, it adds capital complexity. Developers now routinely perform granular nodal studies and congestion forecasts. Lenders, too, increasingly demand curtailment modelling and revenue sensitivity analysis. Without grid investment to relieve bottlenecks, curtailment will remain a defining feature of the Philippine renewable landscape.

Merchant Trading in WESM

Going fully merchant grants developers’ exposure to WESM’s price signals and operational flexibility. Projects can sell power at prevailing spot prices and capture upside during periods of tight supply or fossil fuel volatility. However, this route comes with maximum exposure to market and nodal price volatility.

WESM price movements are driven by supply-demand imbalances, outages, and fuel price swings. During recent dry spells and coal import disruptions, prices spiked above 8 ₱/kWh. Conversely, periods of excess generation—especially solar—can drive prices close to zero. As more solar enters the system, price cannibalisation during midday peaks is a growing concern, steadily depressing solar capture prices over time.

Figure 3: Aurora’s forecast on intraday price shape in Luzon (redacted)

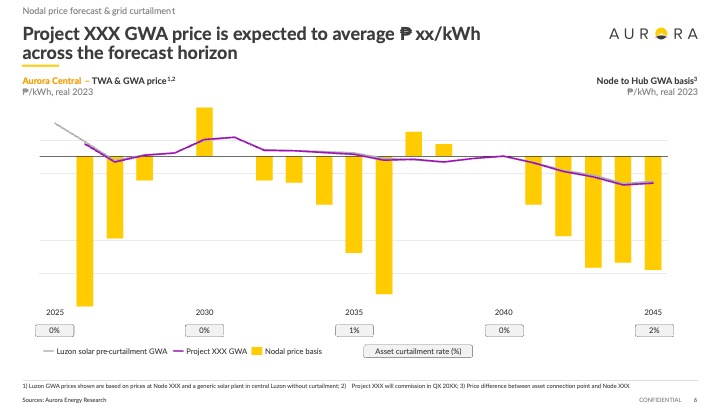

Nodal price risk further complicates revenue forecasting. WESM’s LMP structure means local prices can diverge significantly from system-wide averages. In congested areas, renewables may consistently clear at a discount or face economic curtailment. Without forward hedging tools or a strong balance sheet, pure merchant exposure can undermine project viability.

Figure 4: Sample nodal price forecast for a connection node in Central Luzon

Corporate PPAs via Retail Electricity Suppliers (RES)

Corporate PPAs, typically arranged through licensed RES providers, offer developers long-term pricing certainty while helping corporates meet environmental, social, and governance (targets. Contracts are often structured as financial CfDs—generators sell into WESM, and differences between WESM prices and the strike price are settled bilaterally.

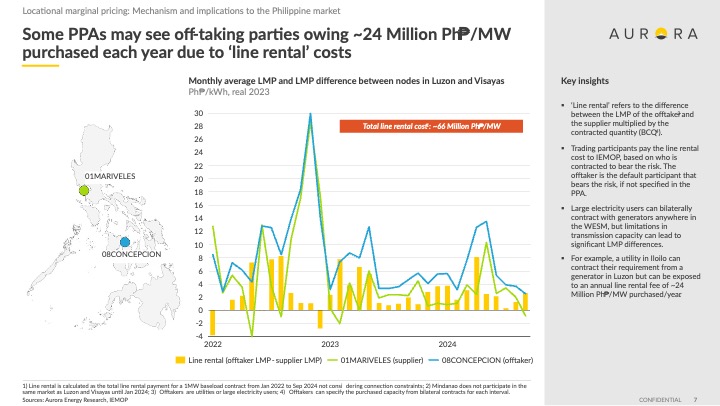

However, these structures shift significant delivery risk to developers. Most CPPAs require sellers to absorb “line rental” costs—the difference between the generator’s node and the offtaker’s node. In practice, this means developers must deliver a net price at the buyer’s location, which can fluctuate due to transmission congestion. Poorly understood basis risk can erode margins substantially.

Figure 5: Line rental case study between a generator’s node in Luzon and an offtaker’s node in Visayas

Furthermore, most CPPAs are “pay-as-delivered,” with no compensation for curtailed volumes. Volume uncertainty thus persists. Contract lengths (5–15 years) are generally shorter than traditional utility PSAs, introducing recontracting risk. Despite these risks, well-structured CPPAs are financeable—particularly with tier-one corporate offtakers—and remain a key tool for diversifying offtake.

Distribution Utility PSAs

PSAs with regulated distribution utilities remain the bedrock of utility-scale renewable financing in the Philippines. Tenors of 15–20 years, underpinned by cost-recovery frameworks and long-term demand forecasts, offer unmatched price stability. PSAs are typically awarded through competitive selection or bilateral negotiation with ERC oversight.

Modern PSAs, however, increasingly include provisions aligning them with WESM’s nodal reality. Generators are often required to deliver energy at the DU’s drawdown node, absorbing any line rental costs. In effect, PSAs are becoming more like CfD-style contracts, where revenue can be diminished by locational basis risk.

Curtailment risk also remains. Unless PSAs include deemed delivered clauses, which are still rare in the Philippines, generators are paid only for dispatched volumes. Therefore, grid-related limitations can reduce realised income. Nonetheless, DU creditworthiness, predictable tariffs, and regulatory support continue to make PSAs the most bankable route.

Green Energy Auction Program (GEAP)

GEAP offers a centralised mechanism to secure 20-year contracts via a competitive bidding process administered by the DOE. Winning projects enter into Renewable Energy Payment Agreements (REPAs) with TransCo, locking in a fixed Green Energy Tariff. For developers, GEAP offers long-duration price certainty, aligning with typical debt tenors.

Yet GEAP is far from a risk-free route. Bidders must post performance bonds (5–20% of project cost), forfeitable upon non-completion. . In essence, developers bear execution risk, construction delay risk, and full operational exposure.

Volume risk is acute. Projects are paid only for delivered energy; any curtailment, whether economic or grid-induced, translates to lost revenue. Moreover, GEAP does not include cost pass-through mechanisms, requiring developers to price risks into their bids. Aggressive underbidding to secure offtake can jeopardise project returns. Despite these challenges, many projects have successfully achieved financial close under GEAP, thanks to the strength of the contract structure once operational.

Figure 6: Overview of GEA-4 requirements

Comparative Assessment

Conclusion

The Philippine power market offers a rich spectrum of offtake options. No path is without risk, but each can be made bankable with the right structuring, pricing, and technical assumptions. Developers must understand not just the contract headline terms, but also how WESM dynamics, nodal pricing, and grid constraints shape actual project outcomes.

The growing importance of curtailment and basis risk underscores the need for rigorous nodal analysis, congestion forecasting, and storage integration strategies. The most successful projects will be those that blend commercial innovation with technical resilience.

Whether navigating the volatility of WESM, the granularity of CPPAs, or the execution discipline required for GEAP, informed decision-making and proactive risk management are paramount. As the energy transition deepens, aligning capital with routes that balance risk and opportunity will define the next wave of investment success.

About the Author

Based in Singapore, Patrick Tan serves as Aurora Energy Research’s Head of Wider Asia, APAC, overseeing Aurora’s products and services across key Southeast and East Asian markets, including Singapore, Malaysia, Vietnam, the Philippines, Indonesia, Thailand, South Korea, and Taiwan. Before joining Aurora, Patrick was a management consultant at Bain & Co., specializing in strategy, operations, and sustainability. To read more of Patrick Tan’s articles and or know more about Aurora Energy click on this link: https://go.auroraer.com/l/885013/2025-05-16/pfnd9?utm_source=commentary&utm_medium=ad&utm_campaign=patrick&utm_id=powerphilippines