Green Tiger Markets PH Electricity May Update

- May 30, 2025

- 0

By Green Tiger Markets

The Green Tiger Markets (GTM) team continues to build on successes. This past month, we passed over TEN MILLION HOURS worth of orders placed that were either matched or in the market for at least 1 day. These orders represent generators looking to forward hedge their offtake or find replacement power. The orders also represent RES looking to manage their load exposures when they don’t have enough supply, or unload excess when they have too much. Thank you to our market participants! We could not have gotten to where we are without you!

We continue to be encouraged by the engagement of our dedicated customers, and I am impressed by the skill with which haggling is taking place. Liquidity is building rapidly as new entrants enter the market and existing players use GTM for a greater proportion of their hedging needs.

Volatility, however, continues to remain the leading ugly characteristic of the WESM spot market. Negative prices were observed for several hours this past month. With all of the solar being energized, we expect to see more volatility to the downside during the midday period.

Areas of Focus for Hedging in May

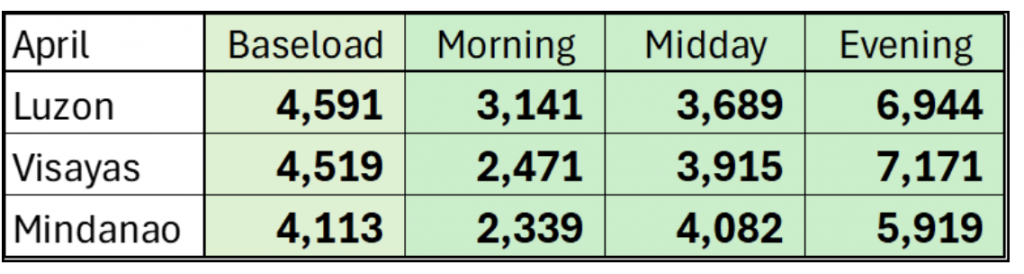

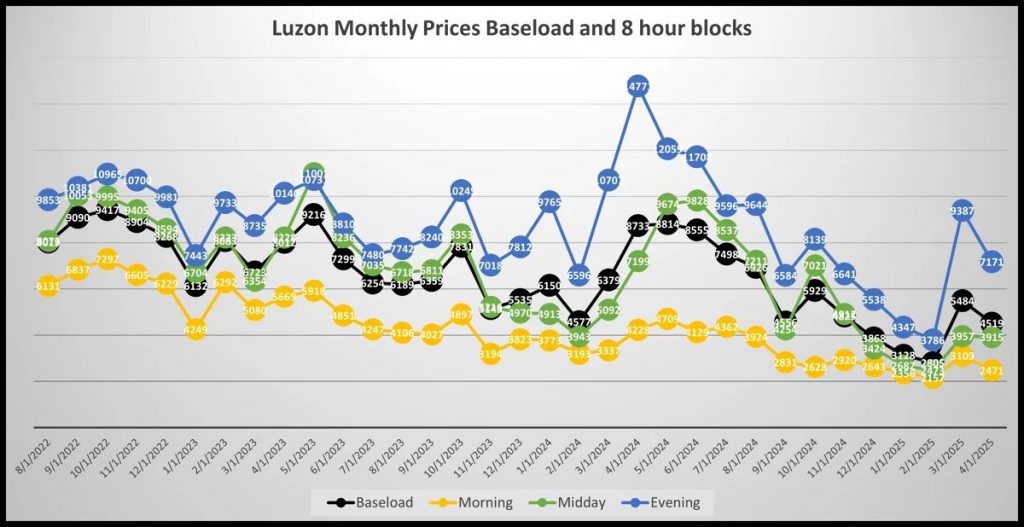

We are working on several orders for 2025 Luzon baseload power, along with interest in our 8-hour blocks, with several parties seeking approvals to go live on indicative matches. Midday hours are generally being offered at 15-25% below baseload prices. Evening hours are generally bid at 140-160% of Baseload. Here are some of the most intriguing opportunities, all values quoted in PHP/MWh:

We’re witnessing an increase in activity from a variety of participants looking to lock in prices for the balance of the year. In general, the bids that we are seeing are quite strong, often well in excess of last year’s prices.

Lastly, we are continuing to quote our first option. We have clients interested in the Q1 2026 Evening hours daily call option struck at 6500. We have aggressive sellers of the option at 1000 PHP/mwh. The option is a net settlement methodology, meaning GTM will calculate the net amount by considering the premium and the payout option for each month. In other words, there is no premium due upfront.

Live pricing levels

As prices continue to fluctuate with changing market dynamics, please contact us directly for the most up-to-date and comprehensive list of orders we are currently handling. Thank you!

Market Data and Commentary

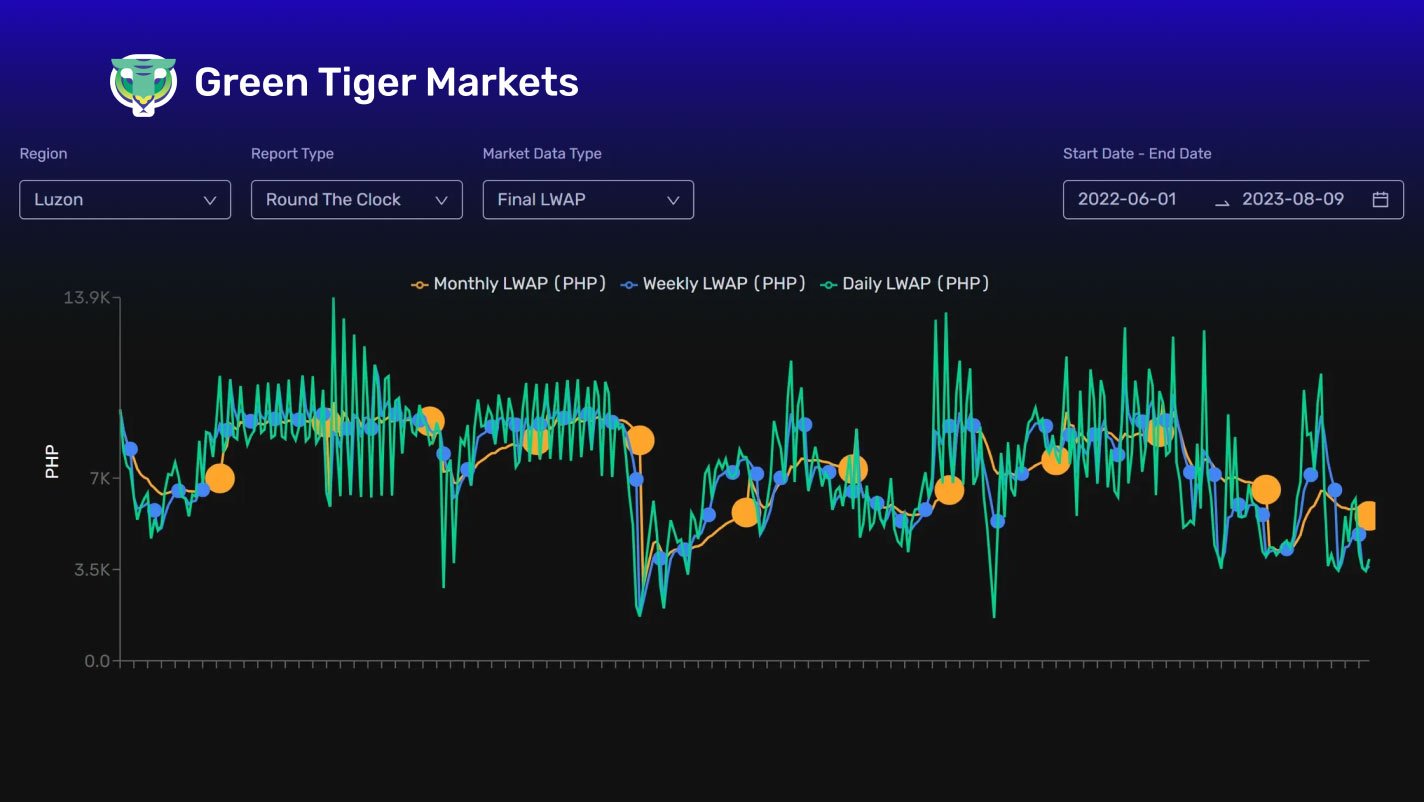

Since our last update, the Philippines electricity sector has experienced notable shifts in WESM, reflecting both market dynamics and structural advancements. In April 2025, WESM recorded a significant price decline, in excess of 15%, dropping to PHP 4591/MWh from PHP 5497/MWh in March, driven by increased supply availability, as reported by IEMOP.

Soggy prices are reminiscent of February prices that put in a monthly low of PHP 2712/MWh, the cheapest since the switch to 5 minute prices. A concerning trend emerged with the third instance of negative average prices across Luzon, Visayas, and Mindanao grids since December 2024, signaling oversupply—likely from solar growth (approximately 2,500 MW of new capacity in the last 36 months)—which could deter investment in new capacity.

Midday prices continue to feel downward pressure and volatility. Daily lows in the month posted NEGATIVE 4285 as the grid was well supplied with plenty of spare capacity and demand dipped for Holy Week and the Easter holiday. It wasn’t all bearish though with March 27th Midday coming in at a stout 6822.

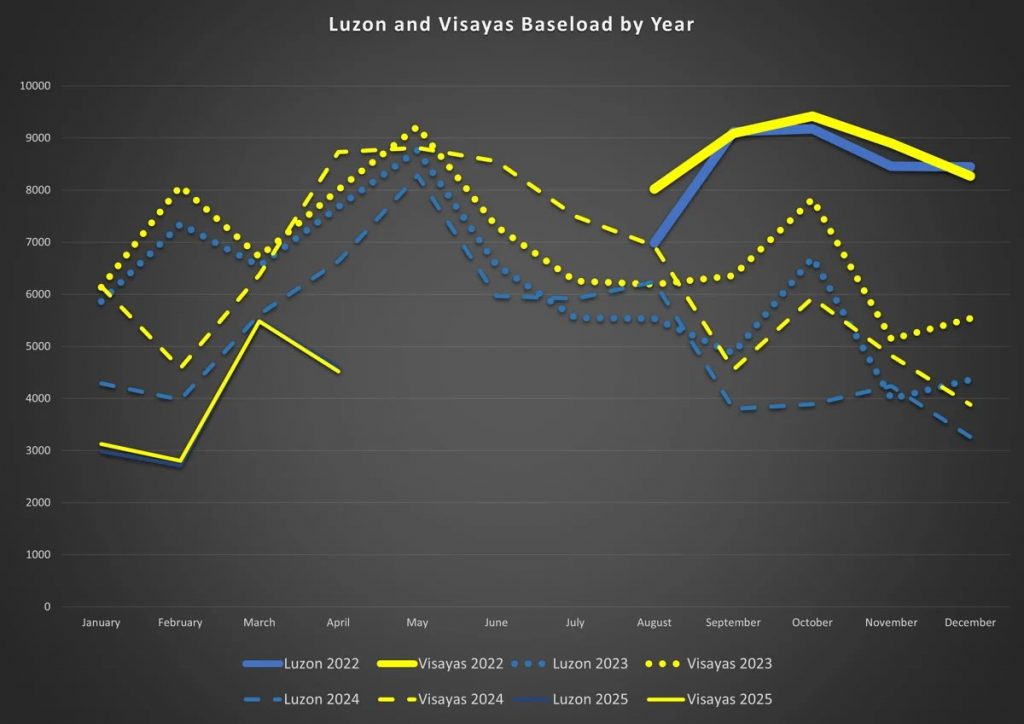

Of note, the spread between Luzon and Visayas has come in dramatically. We were regularly seeing Visayas print 1000 or 2000 pesos over Luzon. The last few months have had them plugged right on top of one another. We were expecting some convergence, but not this quickly, as the grids become more interconnected.

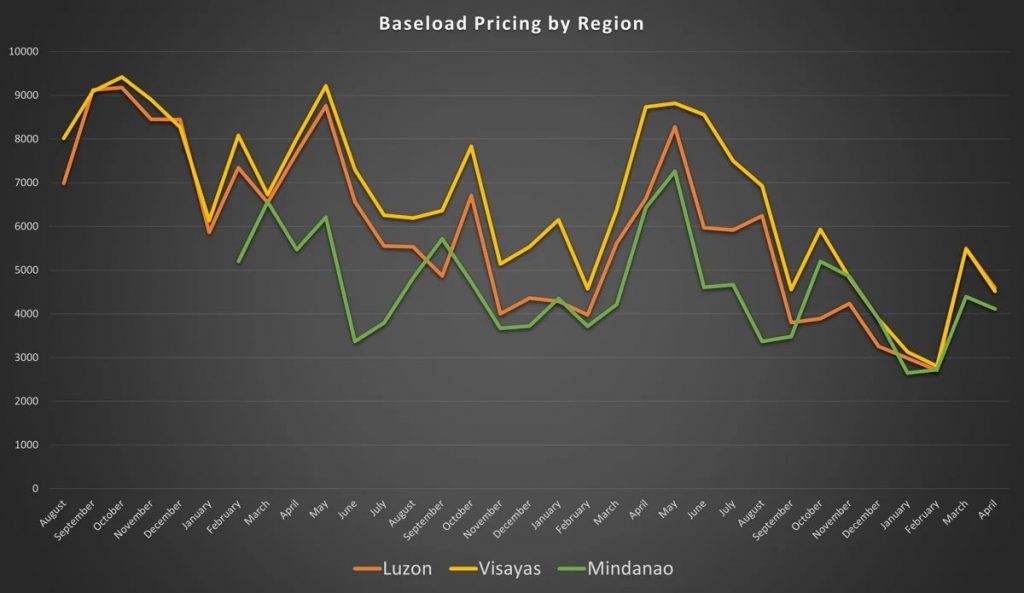

As we step into May, we enter the heart of the summer pricing, however this year, prices have been distinctly soft. Our early look actually has May coming in around 3500 so far, substantially weaker than were the forwards were just a few weeks ago. While the grid will likely be stressed at some point in the next few months, relative to past years, the picture is remains sanguine.

In our second graph below, we have plotted the 8 hour time block contracts as well as Baseload. Evening prices had been headed steadily lower since last Summer, but that trend reversed hard in March. The downtrend resumed in April and will likely persist given the incremental solar coming to the market and the fact that thermal plants will have fewer hours to amortize their fixed costs over. The evening ramp is going to start to look even more like California and Texas.

Midday Hours continue dislocating lower on occasion, with steady repricing for the Midday Hours to match Morning Hours.

Evening hours could see pressure from some of the new gen that is being connected through the balance of the year, but it is a very much wait and see for the evening hours.

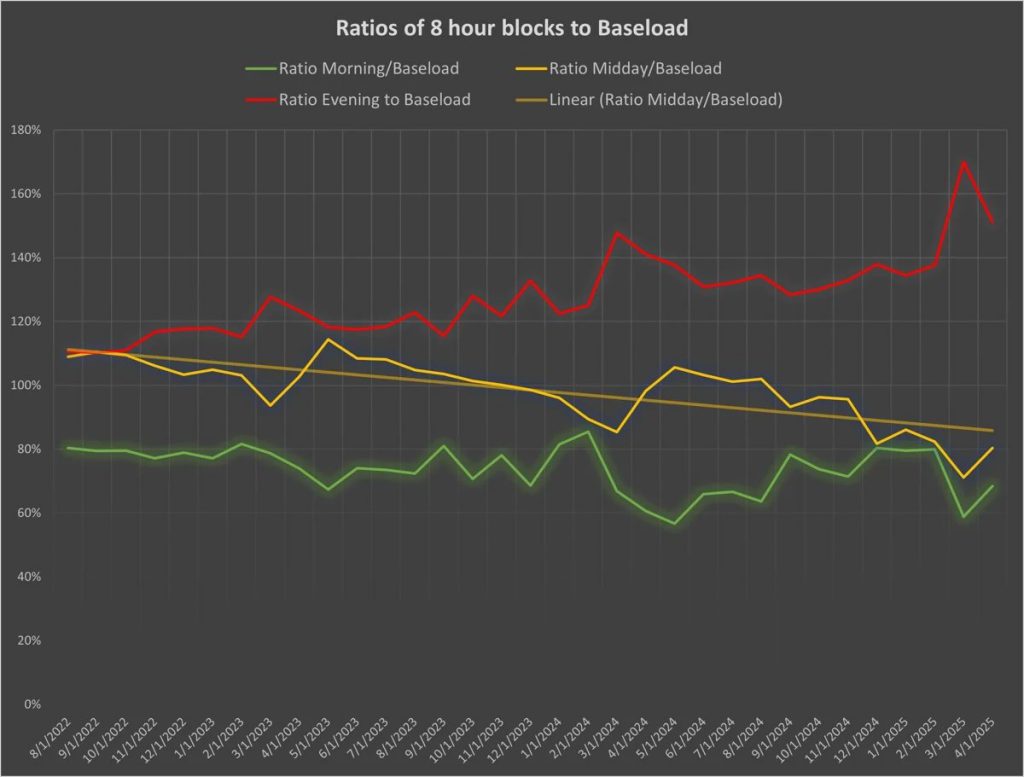

In our third graph below, we have plotted the ratios of the individual 8 hour products along. The trend continues for Evening Hours to diverge and become more “peaky”, though there was a slight retracement in April. The trend continues for Midday and Morning Hours to become more subdued relative to baseload. We are seeing Evening Hours prices clear roughly 70% over baseload for March, and Midday running 25% below baseload. This does not bode well for unhedged solar developers, but could create a massive opportunity for battery operators as well as dispatchable hydro.

If this trend continues, we will see Midday prices close to zero before year end, which could Significantly strain the system.

Year-on-Year comparison

This year is beginning to look significantly different from the last few years. April resumed the weakness after a brief spike in March. During the year, Baseload averaged around 3900, or a full 1200 php below last year. What does this mean for the balance of the year and into 2026?

Hourly Pricing

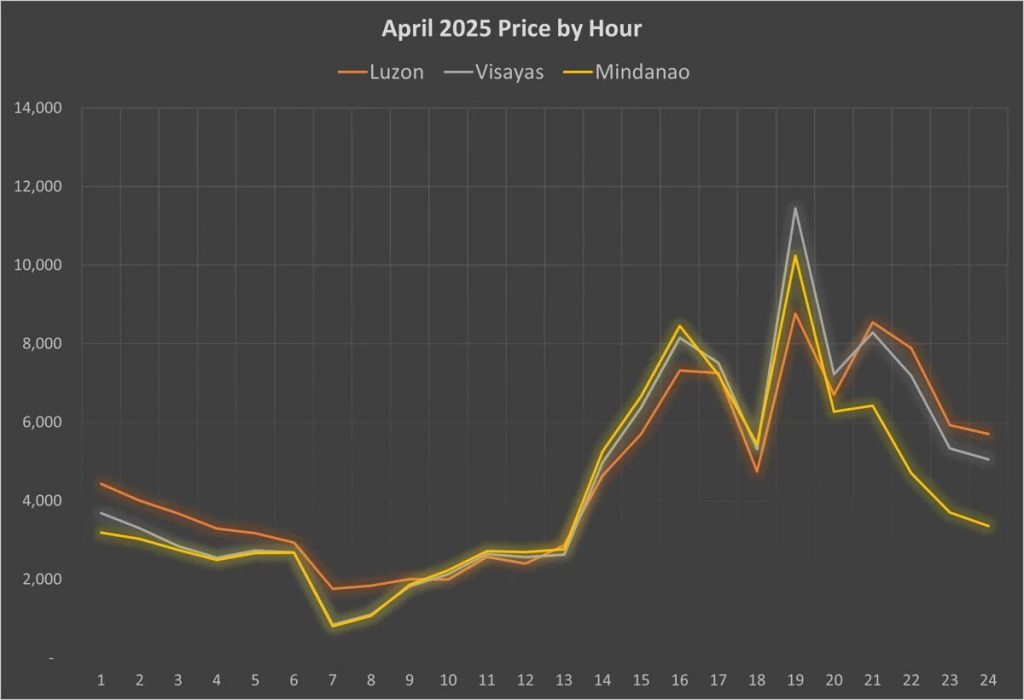

Below we have plotted the various hourly prices by region. Of note, Luzon is over Visayas when its dark out, but generally under when it is light out. This could be explained by the Solar penetration in both regions. Compared to years past, prices were subdued but compared the the first two months of the quarter, we saw an entirely different market.

If you are interested in learning more about our data analysis, please don’t hesitate to contact us at [email protected].

This article was originally published on GreenTigerMarkets.com.