When the sun undercuts the grid

- January 18, 2026

- 0

Electricity is a fickle commodity: it must be produced the instant it is consumed, yet it is

expected to behave—at least for billing purposes—like a stable utility. In the Philippines, where

power prices have long been a political irritant and a commercial handicap, that tension is now

being sharpened by a force that is both welcome and disruptive: cheap solar.

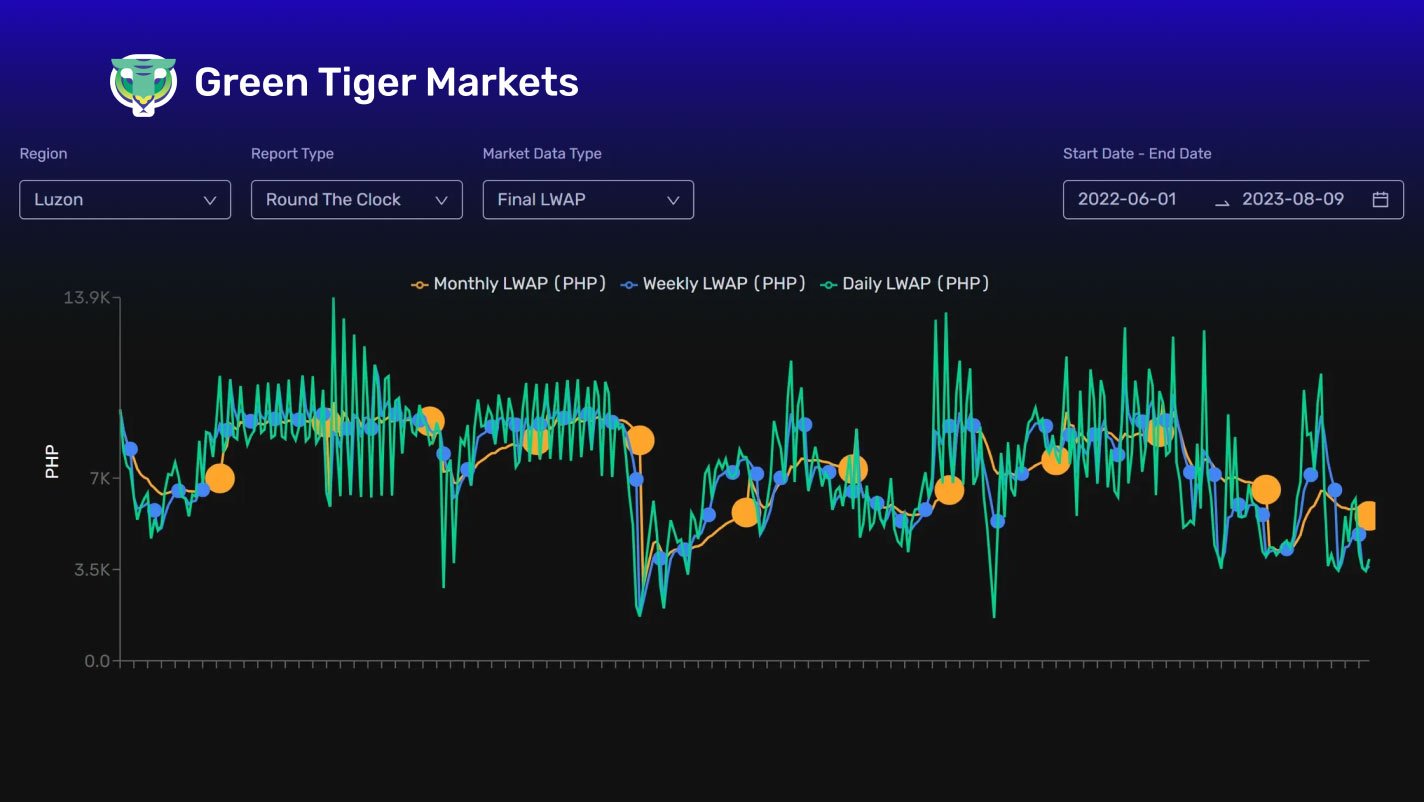

Consider Luzon baseload in 2025. On January 1st 2025, the forward price for calendar-year

2025 baseload sat at PHP 5.25 per kWh. Yet the spot market reality turned out far softer: WESM

baseload averaged about PHP 3.75/kWh for 2025, dramatically below PHP 5.20/kWh in 2024 and

PHP 6.15/kWh in 2023. A power system that investors once viewed as structurally tight suddenly

looked flush.

The causes are not mysterious; they are, in fact, the sort of “good news” that can still unnerve

incumbents. Supply was stronger on several fronts. Installed solar capacity rose, pushing more

low-marginal-cost generation onto the system. A wetter weather pattern than 2024 lifted hydro

output. Imported fuel costs eased—coal and natural gas became less punishing inputs than

they had been during the global energy shock, when coal prices peaked and then later slumped.

Demand, meanwhile, did not play its usual role as the villain. Cooler temperatures reduced

cooling load, industrial demand ticked down slightly, and behind-the-meter solar shaved peak

grid demand.

In other words: more supply, less stress.

But the most consequential story is not the annual average; it is the shape of prices within the day. Solar does not merely add electrons. It changes when expensive plants are needed. The numbers are stark. Midday prices in 2025 averaged 82% of baseload, compared with 96% in 2024. That widening discount is the signature of solar “cannibalisation”: as panels flood the noon hours, they compress prices precisely when they generate most.

This is not a Philippine curiosity. It is a global pattern. Yet the Philippines has a particular reason to take it seriously: WESM—the Wholesale Electricity Spot Market—sits at the heart of dispatch and price formation, operating as a centralised spot market for load balancing. As renewables expand, the spot market increasingly reflects what economists like—marginal costs—rather than what financiers like—stable revenues.

The country’s renewables push has gathered pace. The Department of Energy reported that 794.34MW of new renewable capacity was added in 2024 alone, and that the net-metering programme contributed roughly 141MW over 2015–2024 (with additional “own-use” renewables beyond that). Rooftop solar, much of it unregistered or fast-moving, is also becoming material: one estimate put Philippine rooftop solar capacity at over 1.8GW. Each new panel makes the midday trough deeper and the ramp into evening steeper.

That is where the political economy turns awkward. Falling spot prices are popular in principle. But retail tariffs can remain stubbornly high because consumers pay not only the marginal cost of today’s electrons, but also the legacy of yesterday’s contracts and capacity payments. Reuters reported that spot prices fell to post-pandemic lows in the first half of 2025 amid increased low-cost renewables, even as retail power costs remained elevated and retailers leaned more on the spot market to cut procurement costs. The result is a mismatch between what the system is signalling (abundance at noon) and what consumers feel (still-dear electricity).

The commercial challenge is sharper still. If midday becomes cheap and common, the system will increasingly be priced at the margins: the cloudy day, the windless week, the dry season, the evening peak. In such a world, the most valuable assets are not those that run constantly, but those that can respond quickly: flexible gas, storage, hydro when available, and demand response. Those assets need bankable revenue streams. Yet solar’s very success can make revenue more volatile for everyone—generators included.

This is why the next phase of the Philippines’ power transition will be less about building renewables and more about building institutions that can live with them. Two are missing, or at least under-developed.

The first is flexibility infrastructure. Transmission that can move power from where the sun shines to where demand sits. Storage that shifts cheap midday energy into the evening. Market rules and ancillary services that pay for ramping and reserves. Without these, the system risks an irony: abundant solar capacity alongside recurring tightness at the worst possible hours.

The second is price discovery beyond the spot market—properly scaled forward markets that allow participants to hedge the new volatility. A spot market is excellent at answering one question: “What is electricity worth right now?” But lenders and CFOs ask another: “What will it be worth when my project’s debt service is due?” A functioning forward curve—transparent, liquid, and trusted—turns that uncertainty into a tradable risk. It also disciplines policy: when rules change unexpectedly, the curve reacts immediately.

There are hints of such a market emerging. At Green Tiger Markets (GTM), we have seen a clear uptick in activity, with over 10 million MWh of orders placed in 2025, and order books building across multiple products, with multiple buyers and sellers. While we are encouraged by this activity, what is more important is what our platform makes possible: standardised contracts, efficient matching, and the unglamorous but essential discipline of routine hedging.

Even the early shape of 2026 suggests why hedging will matter. Calendar-year 2026 baseload is starting firmer than January last year, with current Cal-2026 baseload around ₱4.05/kWh—higher than the 2025 spot average, yet still far below the 2023–24 regime. That is exactly the point: the system is not returning to “high” or “low” so much as entering an era of spread—between years, between hours, and between what the sun does and what demand wants.

The Philippines has an opportunity disguised as a headache. If it can pair rapid renewables deployment with flexibility investment and credible forward trading, it can convert solar’s midday glut into an economy-wide advantage: lower costs, less fuel import exposure, and a cleaner grid that remains reliable. If it cannot, it risks a familiar cycle: price collapses that deter investment, followed by shortages that invite intervention, followed by higher costs again.

The sun has done its part. Now the market must learn to trade the shadows.